“Financial peace isn’t the acquisition of stuff. It’s learning to live on less than you make so you can give money back and have money to invest. You can’t win until you do this.” -Dave Ramsey

Retiring young is not a distant dream but an achievable reality with the right steps and strategies. In a world where the typical retirement age seems perpetually out of reach, and achieving a high retirement score is a daunting task, many are asking: how to retire young and enjoy life on their own terms?

Let’s demystify the process of early retirement, breaking down complex financial planning into manageable steps. You’ll learn how to effectively accumulate wealth, manage your finances, and make intentional lifestyle choices that align with your goal of retiring early, plus proving millennials right: they are a lazy generation while you are part of the hard-working ones.

Whether it’s through savvy saving, strategic investing, adopting a minimalist lifestyle, or creating multiple income streams, we’ll provide you with a comprehensive roadmap to fast-track your journey to an early and comfortable retirement.

Key Takeaways

- Set up personal financial goals. Envision and actively plan for early retirement by setting personal financial independence goals, living below your means, and investing wisely to amass the required wealth for a comfortable life post-retirement.

- Think ahead about your healthcare costs. Strategically utilize tax-advantaged retirement accounts, health savings accounts, and diversify income streams to ensure long-term financial security and mitigate healthcare costs prior to Medicare eligibility.

- Adapt your plans if necessary. Regularly reassess and adapt your financial plans to life changes, manage and eliminate debt effectively, and employ smart withdrawal strategies to maintain financial stability and enjoy a minimalist, satisfying retirement lifestyle.

Dream of Retiring Early? Here’s How to Make It Happen!

Imagine a life where you’re free from the daily grind, exploring new adventures instead of clocking in at 9. For many, early retirement is more than just a dream—it’s a goal they actively pursue with smart investments and savvy financial planning.

This isn’t just about buying fancy cars or living luxuriously. It’s about having the freedom to choose how you spend your days. With the right strategies, retirement becomes a time for creativity, personal growth, and unique experiences.

Join us on a journey to learn how you can achieve a comfortable and secure early retirement. Let’s make your dreams of freedom a reality!

Envisioning How to Retire Young

Imagine a scenario where retirement isn’t just a far-off stage of existence but something you could bring closer to your life timeline. The key lies in understanding that the perfect age to retire is not an unchangeable marker but rather an individual decision.

It hinges on reaching financial independence, which empowers you with the freedom to dictate how you use your daily hours—be it persisting in gratifying employment or delving into newfound interests.

This goal revolves around breaking free from traditional constraints and entering a space where time is truly at your discretion.

Estimating Future Needs

Want to Enjoy a Worry-Free Retirement? Start Planning Now!

To turn your retirement dreams into reality, you need to know how much you’ll need. Aim to save enough to cover about 80% of your current income. This gives you the freedom to enjoy life after years of hard work.

Keep your housing costs in check—no more than 40% of your income should go towards it. Paying off your mortgage or downsizing can be smart moves.

if you have a solid financial plan, you can ensure a comfortable retirement and make it even better than your working years. Managing your retirement fund well is the secret to a happy, stress-free future!

Laying the Groundwork for Early Retirement

The cornerstone of achieving early retirement lies in crafting a strong plan that hinges on altering your outlook as well as implementing practical economic measures. It involves adopting a lifestyle focused on:

- prioritizing saving and investing ahead of instant gratification

- making thoughtful decisions about where money is spent

- spend less to stay within, or below, your income level

- enhancing income via side projects or multiple revenue streams

Initiate this process today.

By being smart with your money and saving diligently, you can move closer to financial independence and even retire earlier than expected. Following the principles of the Financial Independence Retire Early (FIRE) philosophy can speed up reaching these goals.

Assessing Your Current Financial Health

Before you start planning for early retirement, it’s important to assess your financial situation thoroughly. Calculate your net worth by adding up everything you own and subtracting any debts.

This gives you a clear picture of where you stand financially.

Review your spending habits to identify areas where you can cut costs. This helps you fine-tune your personal finances and make progress towards your retirement goals.

Establishing a Robust Savings Plan

A smart savings plan is key to reaching early retirement. Start by using the 50/30/20 rule to divide your after-tax income wisely. Make sure to prioritize building an emergency fund that covers three to six months of expenses.

This strategy helps you handle unexpected events while steadily growing your retirement savings.

Embracing a Frugal Mindset

Choosing to live frugally isn’t just about cutting costs—it’s about maximizing value. Differentiate between needs and wants, focusing on what truly enhances your life.

By spending wisely and staying within your budget, you can allocate more money towards retirement savings.

This disciplined approach to money management may help you achieve early retirement and ensure a secure future by boosting your savings.

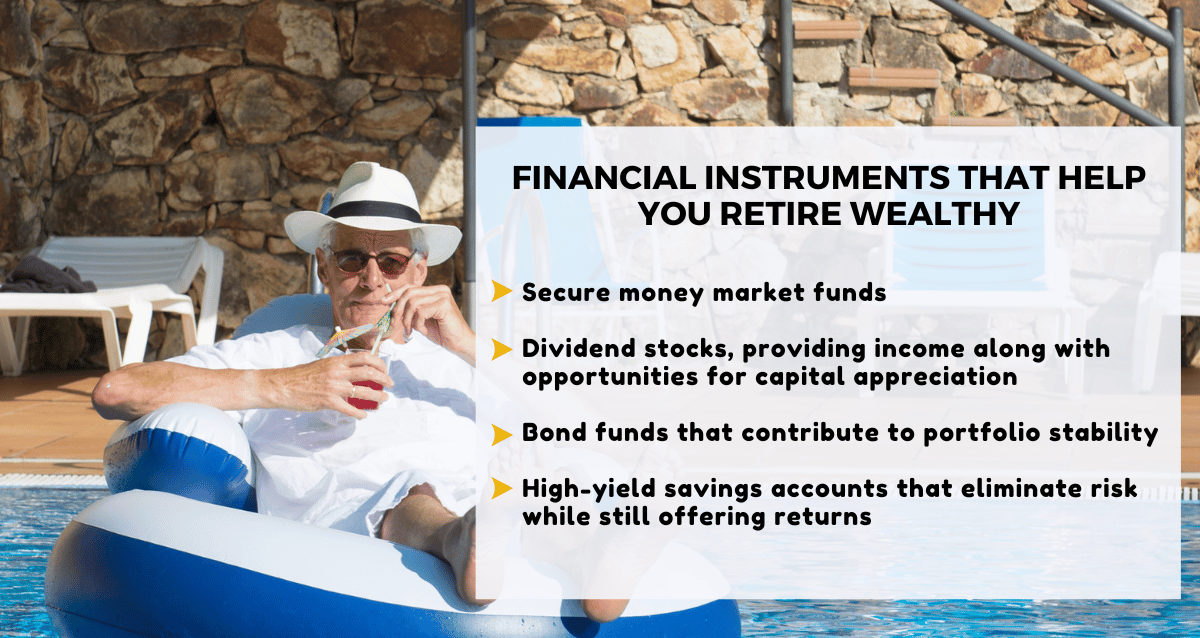

Investment Strategies for Early Retirees

How do you sufficiently cover your early retirement outlays? You have access to an assortment of financial instruments and investment accounts, such as:

- Secure money market funds

- Dividend stocks, providing income along with opportunities for capital appreciation

- Bond funds that contribute to portfolio stability

- High-yield savings accounts that eliminate risk while still offering returns

Construct a diversified portfolio through a brokerage account designed to harmonize expansion with protection of capital.

Maximizing Tax-Advantaged Retirement Accounts

Boost your retirement savings by using tax-advantaged accounts like Roth IRAs. Understanding the rules for tax-free withdrawals and converting to a Roth IRA can give you the best tax benefits.

This approach not only secures your financial future for retirement but also reduces the taxes you owe, allowing you to keep more of your hard-earned money.

Diversifying Income Streams

To build a solid income foundation for early retirement, it’s crucial to have multiple revenue streams. Consider these options:

- Invest in Rental Properties: Create a steady flow of passive income by owning rental properties.

- Leverage Pension Funds and Annuities: These can provide reliable financial security.

- Diversify Investments: Spread your money across stocks, bonds, and mutual funds to balance risks and returns.

- Explore Side Gigs or Freelance Work: Generate extra earnings with additional work on the side.

Having various income sources ensures you maintain your lifestyle without financial worries. Always be on the lookout for new opportunities to grow and secure your wealth.

Planning for Healthcare and Insurance

A critical component of preparing for early retirement involves addressing healthcare requirements before you qualify for Medicare. When moving on from coverage provided by your employer, it’s imperative to account for the entire expense of health insurance premiums in your financial planning.

By foreseeing these costs and adapting your plan for retirement, you can ensure that you maintain financial stability throughout your later years.

Exploring Health Insurance Options

Here are a few pathways to consider regarding your health insurance options:

- Join your spouse’s employer-sponsored plan: If your spouse has a job that offers health insurance, you might be able to get coverage through their plan.

- Use the health insurance marketplace: You can find various plans and possibly get financial assistance through the Marketplace.

- Look into private insurance: Private plans offer a wide range of options, though they might come at a higher cost.

Evaluate all these options to find the best health coverage for your needs during retirement.

Health Savings Accounts (HSAs)

Do you have a high-deductible health plan? If so, consider using a Health Savings Account (HSA). HSAs offer a smart way to save for medical expenses by giving you tax deductions on contributions and allowing your savings to grow tax-free.

HSAs are a great tool for managing healthcare costs in retirement, providing both financial benefits and flexibility.

Navigating Social Security and Retirement Benefits

Understanding Social Security and retirement benefits is crucial for those planning to retire early. Here’s what you need to consider:

- Weigh tax implications: Social Security benefits have tax consequences, and it’s important to know how these will affect your retirement income.

- Strategize for maximum income: To get the most out of your benefits, you need to carefully plan your timing and approach.

If you’re thinking about retiring early, choosing when to start your Social Security benefits is key. You can start as early as 62, but this means smaller monthly payments. If you wait, you can get much higher payouts.

It’s all about balancing the need for immediate income with the benefits of waiting.

Incorporating Pension Funds or Annuities

Annuities and pension funds can provide a steady income stream during retirement, helping to bridge the gap between your expenses and savings. Here’s how you can make the most of them: Explore different annuity options.

Whether you choose an immediate annuity for instant income or a deferred annuity to start payments later, you can tailor your income plan to fit your specific needs.

These financial tools ensure you have continuous support throughout your retirement years, giving you peace of mind and financial stability.

Dealing with Debt Before Retiring Early

Having debt, particularly the kind that comes with high interest rates, such as those from credit card balances, can significantly hinder your ability to retire early. To prepare for a successful retirement, it is essential to focus on paying off these debts and ensure you do not accumulate new ones.

Adopting this strategy will allow you to enter into retirement enjoying financial freedom, allowing you to fully appreciate the benefits of your diligently built up retirement nest egg without the burden of debt.

Prioritizing Debt Repayment

To liberate yourself from the constraints of financial liabilities, prioritize eliminating debt on credit cards with high interest. Addressing these debts expeditiously not only saves money over time but also propels you toward achieving your objective of an early and relaxing retirement.

Refinancing and Consolidation Options

Consolidating debt and refinancing can serve as potent tools for diminishing both the interest rates you pay and your monthly outlays. This applies whether it’s regarding a home loan refinance or handling educational debts, which may help in organizing your finances more efficiently to facilitate plans for early retirement.

Adjusting Your Retirement Plans Over Time

As life unfolds, it’s crucial to keep your retirement strategy flexible and up-to-date. Ensure that your plans continue to be effective by routinely reassessing and modifying them in response to any shifts in income, family circumstances, or health conditions.

Staying adaptable will aid in preserving financial security during your retirement years.

Embracing a new chapter of life, such as retirement, often entails making adjustments to your living situation. Opting for a more compact and manageable home can lead to substantial savings on your living expenses, ensuring that you continue to enjoy comfort during your later years.

Reevaluating Investment Returns

Regularly checking your investment returns is crucial to ensure they meet your retirement goals. If your investments aren’t performing as expected or your financial situation changes, it’s time to make adjustments.

Staying alert and actively managing your investments helps keep your retirement savings growing steadily. This vigilance ensures you’re always on track to reach your financial goals.

Staying Informed on Tax Laws

Keeping up with ever-changing tax laws, especially those related to income taxes, is crucial in retirement. Changes can significantly affect how much money you keep or payout.

Regularly consult with a financial advisor and keep an eye on IRS updates. This way, you can take advantage of all possible tax benefits and protect your retirement savings from unnecessary taxation.

Creating a Withdrawal Strategy

Crafting a savvy strategy for pulling funds from your savings is vital to ensure the longevity of your money during retirement. Grasping the tax consequences tied to different account withdrawals and formulating a blueprint that reduces taxes and avoids early withdrawal fines on your nest egg when you extract cash is essential.

Balancing Withdrawal Rates and Nest Egg Preservation

Utilizing the 4% rule is a widely adopted strategy for determining a withdrawal rate from your retirement savings that can help maintain your nest egg over time. Yet, it’s crucial to tailor this percentage to fit individual needs and current market dynamics.

Vigilantly monitoring both your expenditure and how well your investments are doing is critical in ensuring that your savings endure throughout retirement, preventing you from depleting them prematurely.

Considering Bridge Accounts and Roth Conversion Ladders

If you retire before reaching the standard retirement age, utilizing bridge accounts and Roth conversion ladders allows for the use of your retirement savings without suffering penalties for early withdrawal. Through a calculated transfer of funds from a traditional IRA into a Roth IRA incrementally, it’s possible to establish an income stream during retirement that is both tax-efficient and available as required.

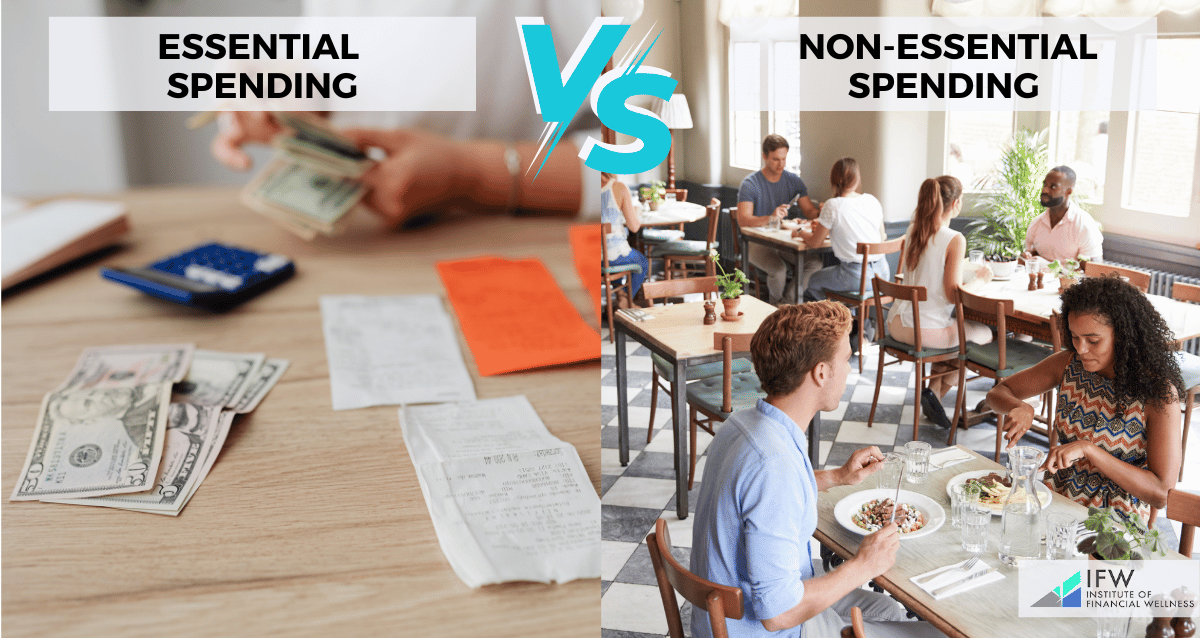

Embracing a Minimalist Approach to Retirement Spending

By focusing on the most valuable experiences and adopting a minimalist approach to retirement spending, you can remove unnecessary expenses. This allows you to stretch your savings. And live comfortably with less, thereby relishing the liberty that financial independence provides.

Embracing minimalism involves distinguishing between spending that is necessary and what’s not. Necessary expenses are those that cater to basic life needs, whereas non-essential spending entails optional purchases which can typically be trimmed or completely cut out.

Concentrating on the aspects that truly enhance your life allows for a simplification of your financial situation, giving precedence to the accumulation of savings for retirement.

The Impact of Downsizing

Adopting a more modest way of living can greatly enhance your prospects for early retirement. To achieve this, consider the following downsizing tactics:

- Opt for a cozier residence

- Choose an economical vehicle

- Eliminate superfluous spending

- Slash recurring monthly charges

- Streamline your clothing collection

- Declutter your home environment

Such adjustments enable you to drastically lower your expenses each month, thereby accelerating savings accumulation for retirement.

Pursuing this approach offers not just monetary gains but may also cultivate a simpler and more rewarding lifestyle.

Empowering Your Retirement Journey: Unleash Your Financial Potential with the Institute of Financial Wellness

The Institute of Financial Wellness stands as a comprehensive repository for financial knowledge, tools, and advisory services to navigate your journey towards retirement with assurance. We help those looking to enhance their retirement savings strategies, decipher insurance products, or keep abreast of the newest fiscal developments, positioning ourselves as a premiere destination for all financial inquiries.

A myriad of beneficial offerings is accessible through IFW, including:

- Equipping individuals with the acumen required for prudent fiscal decisions

- Connecting you with seasoned experts in finance

- Offering guidance throughout every segment of your monetary life cycle

- Providing unwavering support tailored to help fulfill your aspirations concerning retirement

Entrust yourself into the care of IFW where an optimal lifestyle can be realized while seizing maximum advantages from your economic pursuits. With educational sessions, such as the Retirement Score Webinar, you can better understand whether you are on the right path to retiring early.

Full Summary

We’ve journeyed through a landscape of strategies and insights designed to pave the way for an early and comfortable retirement. By embracing frugality, making smart investments, and planning for healthcare and tax implications, you can defy stereotypes and retire on your own terms.

Remember, the key to success is not just in the planning but in the ongoing adjustments and the determination to see your vision come to life. So go forth, armed with knowledge and inspired to build the retirement of your dreams.

Frequently Asked Questions

Is $4 million enough to retire at 40?

Certainly, having $4 million saved up makes it quite possible to retire early at the age of 40.

Initiate your retirement planning now and prepare for an early exit from your career!

What is the best age to retire early?

Typically, the optimal age range for early retirement is considered to be 41-45 years old. This period enables one to take full advantage of good health and a high level of enjoyment from life after dedicating approximately two decades to diligent saving and investing.

Relish in the hard-earned leisure of your retirement!

How can I estimate how much I need to retire comfortably?

In planning for a comfortable retirement, it’s advisable to calculate your retirement budget at roughly 80% of your pre-retirement income while making adjustments for foreseeable expenses. Incorporating a buffer of about 10-20% will allow for greater financial flexibility during retirement.

Are there any strategies to access retirement savings early without penalties?

Yes, you can utilize strategies like Roth IRA conversion ladders and bridge accounts to access retirement funds early and avoid penalties.

Start planning for your early retirement savings today!

How can I ensure my healthcare needs are covered in early retirement?

To secure coverage for medical expenses during early retirement, it’s important to investigate whether you can obtain health insurance through your partner’s workplace plan or seek options available via the Health Insurance Marketplace. Look into the possibility of establishing a Health Savings Account (HSA) should you qualify.

It is crucial to meticulously explore these alternatives in advance of finalizing any decisions regarding your healthcare provisions after retiring.

What is the average age for retirement in the US?

The average age of retirement has increased over time, up from age 57 in 1991 [1].

Does the current life expectancy affect Americans’ retirement?

The current U.S. life expectancy is 79.1 years, up +16.15% from 68.1 in 1950. This means Americans are living longer and must save more for retirement [2].

How many people will likely retire in 2024?

22% of working Americans are likely to retire in 2024 [3].

Related Articles

Traditional IRA vs. Roth IRA

Traditional Individual Retirement Accounts (IRA), which were created in 1974, are owned by roughly 36.1 million U.S. households. And Roth IRAs, created as part of the Taxpayer Relief Act in

Peter Foldes

Nov, 10 2021

Tax Efficiency in Retirement

Will you pay higher taxes in retirement? It’s possible. But that will largely depend on how you generate income. Will it be from working? Will it be from retirement plans?

Peter Foldes

Nov, 10 2021

Consider Keeping Your Life Insurance When You Retire

Do you need a life insurance policy in retirement? One school of thought questions this decision. Perhaps your kids have grown and the need to help protect the household against

Peter Foldes

Nov, 10 2021